Last September, President Donald Trump heralded the idea that public companies have the option to report earnings twice a year rather than every quarter.

It’s a proposal that has come up before as a way to better serve public companies, including from the president himself during his first term. Now, the idea is picking up steam: The Wall Street Journal reported in March that the Securities and Exchange Commission (SEC) may soon issue a new rule allowing public companies to shift to semiannual reporting (opens a new window).

Proponents of the idea say that preparing quarterly earnings reports, known as Form 10-Q filings, requires significant time and expense. Less frequent reports would allow management teams to focus on long-term strategies rather than chasing short-term results to meet or beat quarterly earnings expectations. And it may offer additional encouragement to private companies that are on the fence about going public.

But there are risks to consider. Fewer disclosures could increase exposure for directors, officers, and the companies they serve in an environment of aggressive shareholder litigation and growing investor expectations for transparency.

The regulatory burden argument

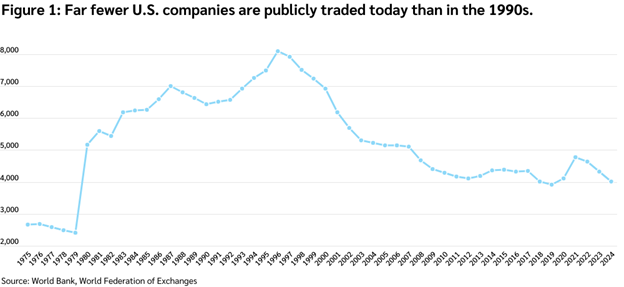

The number of publicly traded companies in the U.S. has shrunk by half compared to the 1990s (opens a new window), according to the World Bank and World Federation of Exchanges. (See Figure 1.)

Many companies remain private for various reasons. Many companies say the cost and burden of quarterly reports — assembling financial statements, narrating management discussion, and conducting internal compliance and review — cause them to avoid going public.

Studies say regulatory compliance costs consume a meaningful portion of corporate value. A 2025 study by Columbia Business School found that regulatory compliance costs for the median U.S. company account for 4.3% of its market cap (opens a new window). The burden falls more heavily on smaller companies, who's typically limited internal resources often mean they pay to outsource these services.

Supporters of semiannual reporting say fewer reports could reduce pressure on public companies without shortchanging investors, particularly given that publicly traded companies in the United Kingdom, European Union, and Australia can report earnings twice a year.

Risks of semiannual reports

Companies that welcome semiannual reporting should be mindful of potential risks. The SEC proposal will likely give companies the option, rather than the mandate, to report semiannually. That choice opens an avenue for shareholders and securities class-action attorneys to scrutinize the optics of any corporate actions that follow.

Less frequent disclosures mean those that are made will attract a more critical eye. Plaintiffs’ counsel will likely assert that material information that may have surfaced earlier in a quarterly reporting cycle remained improperly undisclosed for longer. Arguably, the longer information remains out of the market, the more shareholders are affected by any stock price swings.

These risks carry weight in an environment where securities lawsuits have evolved beyond straightforward accounting misstatements to external factors impacting company performance. Plaintiffs’ counsel now view disclosures, like the occurrence and magnitude of cyberattacks, with greater scrutiny. More recent developments, such as geopolitical tensions, supply chain disruptions, and tariff-related complications, have created another fruitful avenue for securities plaintiffs to pursue.

Exposures from other types of disclosures

Companies that report semiannually may want to, or feel pressure to, meet investor and analyst demand for information. They may accomplish this through press releases, investor days, conference presentations, or other public communications. These less formal communications pose a risk of inadvertent material misstatements, inconsistent messages, or overly optimistic performance projections, all of which could be cited in a securities lawsuit if they influence stock price movements.

Semiannual reports can also affect stock trading blackout periods for company insiders. Longer blackout periods can increase the risk that shareholders or regulators will assign improper motives to insider trades, even if they’re innocent or inadvertent.

Aside from these risks, some companies cannot switch to semiannual reporting, even if they want to. Companies may face debt covenant terms and other lender requirements that necessitate more frequent reporting. Others may have to answer to shareholders and analysts who demand more frequent updates, such as through voluntary 8-K updates.

It’s also worth noting that many Financial Times Stock Exchange 100 and other non-U.S. companies still issue quarterly reports, even though it’s not mandatory, due to market demand.

Practical considerations for directors and officers

There’s broad support in the current administration for the SEC’s forthcoming rule, which means it’s not too soon for companies to consider their options and discuss whether to make any changes with outside legal counsel. It’s also worth discussing the implications of changing the reporting cadence for directors and officers (D&O) insurance coverage, particularly the impact less frequent reporting may have on underwriters’ perception of the organization’s risk profile, as well as any changes that need to be made to the renewal cycle, with an experienced insurance broker.

While semiannual reporting may ease regulatory burdens, it could heighten disclosure risk in an environment where investors, regulators, and plaintiffs’ attorneys increasingly expect timely, granular insight into corporate performance.

For more information, visit our D&O insurance page here (opens a new window).