Skip to main content

Explore Lockton’s comprehensive quarterly market update for commercial insurance. Get insights on rate trends, inflation, emerging risks like AI and parametric solutions, and sector-specific analysis for construction, energy, architecture, and logistics.

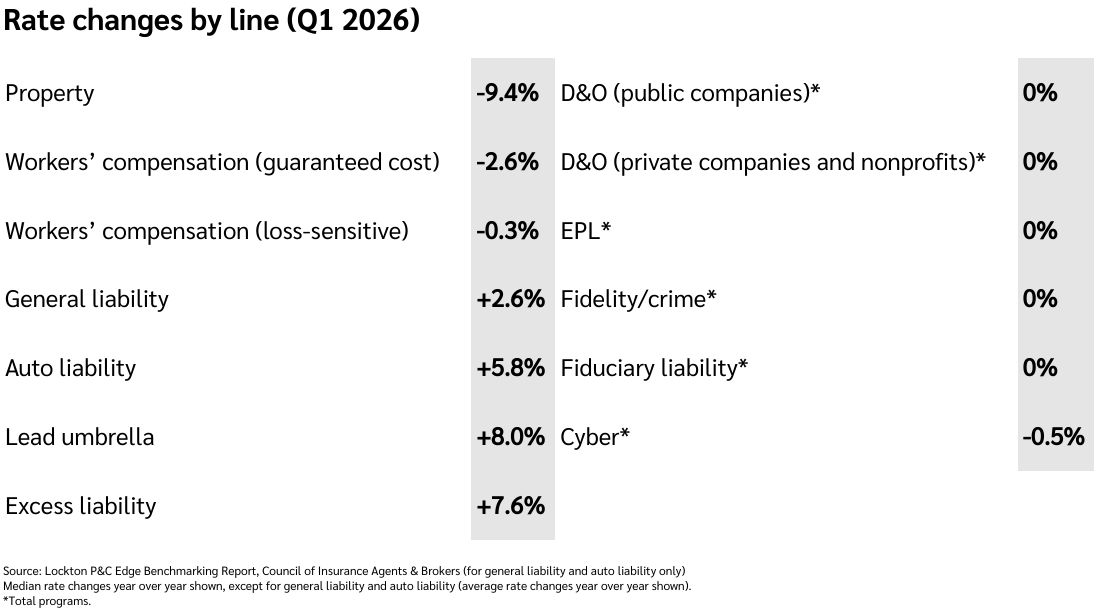

A time to strike

For insurance buyers, the market outlook remains broadly favorable, although conditions vary by line. Organizations have a window of opportunity to strengthen risk and insurance strategies before conditions evolve. Rather than sitting back, the best insurance buyers rethink program structure, test alternatives, and strengthen carrier relationships before conditions change again.

Previous market updates