The threat posed by flooding to UK insurers’ profitability is nothing new. Nor are the headaches this causes for property owners looking to insure their portfolios. But the specific threat from surface water hazards has emerged recently as a major concern.

Severe weather driven by climate change, and how it plays out across particular local geographies, has combined with decisions made by urban planners and developers to make surface water hazard a noticeably more prevalent peril in town and city centres and a growing exposure for urban property portfolios.

The cumulative effect of incremental changes to our urban centres over time came vividly to light during London’s 2021 flash floods, and again, early this year, with the chaos caused by Storms Eunice and Franklin right across the UK.

In London in particular, the creeping disappearance of gardens in an urban environment dominated by impermeable surfaces, has left rainwater with nowhere to go when heavy downpours strike. The capital’s drainage system was designed for a city of four million people. As London’s population continues to grow, that system is currently working 80% over capacity. Victorian drains simply cannot cope with sudden deluges.

Nor are these problems unique to London. We’re seeing similar problems more and more often wherever high population density and intensive development come together in towns and cities up and down the UK.

An additional exacerbating factor in London is the city’s mania for adding basements to both new and existing properties and refurbishing existing subterranean spaces. This is an increasingly prevalent phenomenon throughout the capital city, affecting both residential and commercial properties. Basement levels are more prone to flooding, due to their proximity to underground pipes and drains and the obvious fact of their being below street level.

Types of flooding

There are three main types of flooding likely to impact real estate insurance:

Fluvial

More commonly known as a river flood, this occurs when rising water levels in a river, lake, or stream rise cause it to overflow surrounding banks, shores and neighbouring land. This typically arises as a result of heavy rainfall or snowmelt

Pluvial

This occurs when an extreme rainfall event creates a flood independent of any overflowing body of water. The two most common types of pluvial flood are surface water floods and flash floods

Coastal

When land near the sea or an estuary is inundated by seawater, this is coastal flooding. It commonly occurs when windstorm events coincide with high tides.

In this article we focus purely on pluvial flooding (from pluvia, the Latin word for rain).

The impact on insurers

Statistics from last year’s summer floods in London compiled by our internal claims team illustrate the dramatic impact flash floods can have. Examples like this help explain why insurers have modified their underwriting strategies.

On 12 July 2021, 63 claims were submitted to our team, totalling £3,254,500. A further 15 claims were also submitted that week. Eight of the total 78 claims were deemed ‘major losses’ as they were over £100,000. Two of the eight major losses exceeded £650,000. The largest was for £688,850, which related to a flooded basement.

Loss adjusters attributed these losses to the West London’s antiquated drainage systems, which were totally overwhelmed by the high volume of rainfall recorded. They also think the area’s intensive urbanisation stopped water being absorbed by the soil.

Insurers’ reaction to increasing surface water flooding

Flood mapping systems

Historically, the way insurers have used flood mapping as a guide to rating has been inconsistent from carrier to carrier, with antiquated and outdated mapping systems still in widespread use due to lack of investment.

With a growing awareness of the impact of climate change in recent years, insurers have tried to improve the risk profiles of their property insurance portfolios. The aim has been to protect profitability by improving premium-versus-claims-paid returns.

To a greater or lesser extent, fresh investment in more sophisticated technology has increased the sensitivity of insurers’ flood mapping systems, helping assisting them in their attempts to reduce the volume and severity of flood claims they’re exposed to. Insurers apply terms based on where a risk is located within their software and the corresponding severity of risk indicated by whatever flood mapping tool they are using.

Surface water flooding - which has only recently become a key concern for underwriters - had not previously come in for detailed scrutiny from these mapping tools. Disparities between the sensitivity of different insurers’ flood mapping systems poses an issue for scheduled risks, as it complicates insurers’ ability to provide comparable terms.

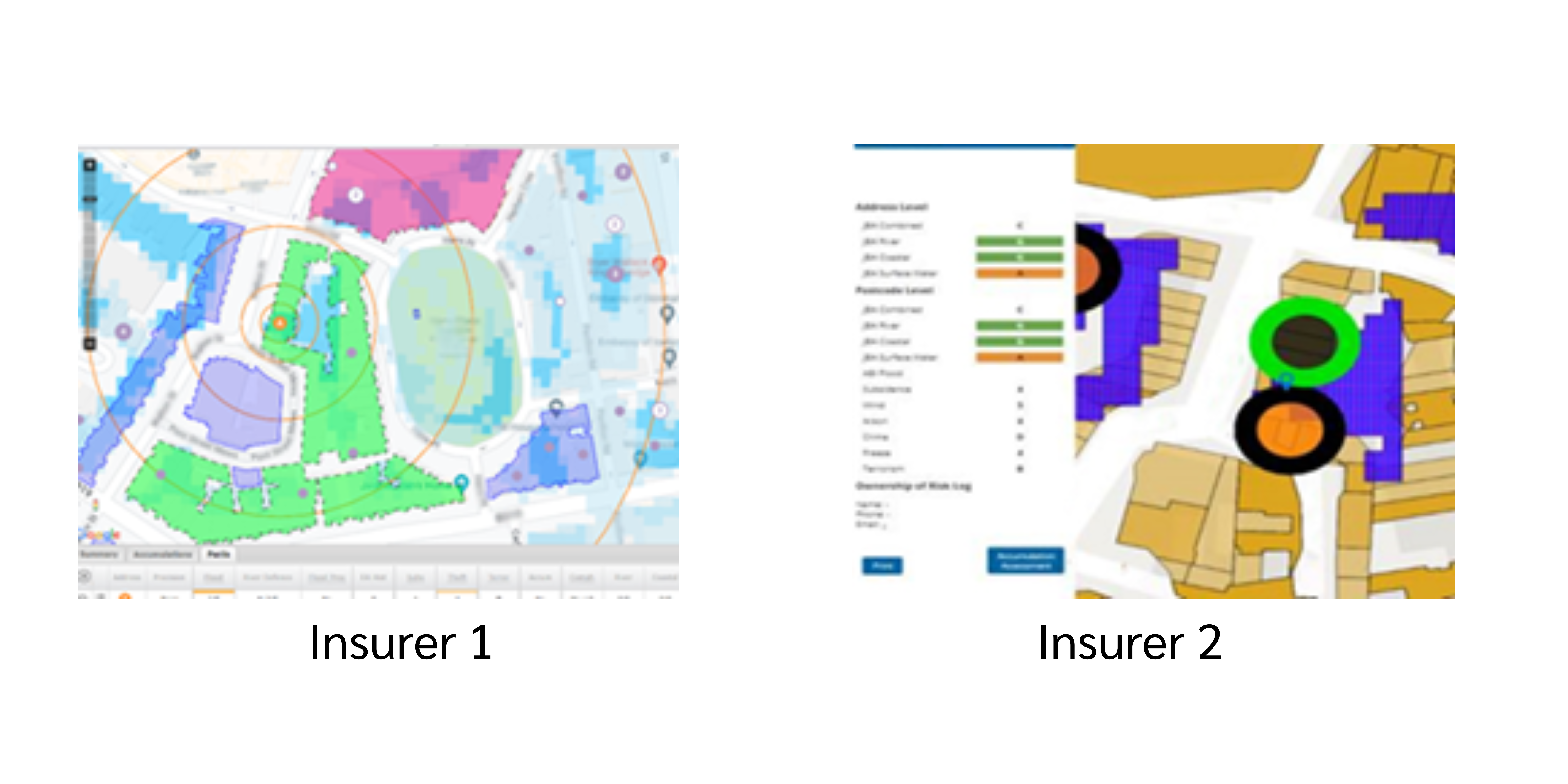

The two screenshots below, taken from two different insurers’ flood mapping software, illustrate this point.

Both insurers deem the flood risk at this location to be ‘medium’ in terms of its severity. However, Insurer 2 quoted a flood excess of £250,000, whereas Insurer 1 quoted just £10,000. We have also seen cases of insurers restricting their limit of indemnity for flood cover for high-risk locations. The example above highlights how widely divergent different insurers’ underwriting strategies can be, depending on how severely they have been impacted by surface water flooding in the past.

Increased deductibles

It is not uncommon for insurers to increase flood deductibles on all risks across their books, particularly for locations that fall within the high flood risk category. We have seen insurers quoting deductibles as high as £250,000, which can be very challenging for us to communicate to clients who may not have realised they were acquiring a property in what would end up designated as a high flood risk area.

The natural flood risk profile of a location may not be immediately obvious, particularly if it is well away from rivers or coastlines. One way we can help alleviate the issue of elevated flood excess levels is by offering our clients the option of purchasing flood deductible insurance. More on this below.

Basements

With basement conversions increasingly commonplace, insurers are acutely mindful of the high reinstatement costs associated with flooded basements and the increased exposures they could face in areas where basements and pluvial flood risk coincide.

Insurers are taking a particularly keen interest in what basements are used for. We have seen cases of split deductibles across a single risk. For example, a higher excess might apply to basement and ground floors, while unmodified cover applies to floors deemed less at a risk of flooding.

Solutions

There are several measures that can be taken by property owners who are concerned about surface water flood risks affecting their portfolio’s claims performance or their ability to purchase affordable flood cover for specific properties. These measures can enable you and your broker to obtain favourable terms from insurers.

Many of our clients have access to risk management funds that we have arranged under their real estate policy. These funds could be used to invest in measures that mitigate flood exposures.

A few examples are:

Soakaways - These are effectively pits filled with stones and gravel covered by a plastic membrane. Typically situated 5-8 metres from a property, they help drain rainwater from pipes by dispersing it back into the soil. This can be helpful for properties that can’t connect to the main drain

CCTV surveys - CCTV surveys can provide footage from inside pipes, allowing clients to deal with any urgent issues at once. For commercial sites, it is advisable to carry out a CCTV survey every three to five years, depending on the surrounding area and changing water table

Gutters and gullies - regularly maintaining gutters and gullies - and keeping them clear of debris - is crucial for a healthy drainage system. Rainwater pipes also need to be kept clear. Doing this after a storm helps ensure that dead leaves don’t start building up and preventing water from draining away safely.

How can we help?

Lockton offers two key insurance policies that can help clients looking for solutions to the problems they are encountering now with traditional flood cover.

Flood excess insurance

As noted above, insurers are increasing their deductibles for locations they deem at a high risk of flooding. Flood excess insurance will cover the cost of any applicable property insurance flood excess up to a maximum of £100,000.

Flood Flash insurance

This non-traditional flood insurance is a parametric cover that offers pre-specified payouts based on a specified trigger event. A Flood Flash sensor is installed for each policy purchased. When the sensor detects flooding at a trigger depth selected by the insured, it sends data to the insurer’s wireless network. Once this data has been verified, the insurer will automatically pay out - removing the uncertainty, cost, and time associated with claiming on traditional insurance policies.

Four Twenty Seven

Lockton is also now collaborating with data research and analysis firm Four Twenty Seven to make market-leading climate data available to Lockton clients. Four Twenty Seven assesses data across six physical climate hazards: heat stress, water stress, slides, sea-level rise, hurricanes/typhoons and wildfires. A better-informed idea of what is coming down the line may not always enable us to avoid risk altogether, but it can certainly help us mitigate it.

To find out more about Four Twenty Seven, the following link will take you to a recent article in our newsletter:

Growing awareness of the risk of surface water flooding has seen insurers adopting a more stringent underwriting approach. But there are plenty of practical measures you can implement to alleviate its impact on your property portfolio. Lockton also offers insurance products that can lessen the financial impact of higher excesses and premiums. Together we can act proactively to manage the impact of this less familiar form of flood risk.

For more information, please contact Roshni Morzaria:

T: +44 0207 933 2309 | E: roshni.morzaria@lockton.com